It was a scene out of a bygone era a few weeks back when ten Republican senators met with Joe Biden in the Oval Office to talk about the COVID relief package. The differences were substantial: $1.9 trillion vs. $618 billion. A trillion dollars is apparently a bridge too far for those ten Republicans. They were all for unity, but it now comes at a price. If unity is what Joe Biden wants, apparently he needs to take things down a bit. Into the billions, preferably.

Decades ago, at a time when humor was still allowed in the nation’s capital, Senator Everett Dirksen commented on how spending federal money can easily get out of control. “A billion here, a billion there,” the Illinois Republican quipped, “and pretty soon you’re talking real money.” It took the better part of a half-century, but ‘trillions’ finally eclipsed ‘billions’ as the metric of serious money in the wake of the 2008 financial collapse. Trillions of dollars lost as a housing bubble burst. Trillions of dollars pumped into the banking system by Congress and the Federal Reserve Bank. And, as things turned out, trillions of dollars of wealth created along the way for the wealthiest Americans.

Maine Senator Susan Collins, who spoke for the group of ten, seemed to be under the illusion that the GOP was still the Republican Party of Everett Dirksen. It used to be the party of fiscal responsibility, that believed that balanced budgets were a moral obligation of leadership, as Dirksen’s quip hinted. But Ronald Reagan put an end to all that, as tax cuts became, along with judges and guns, the raison d’être of the Republican Party. It is not that people should not be concerned about the growing public debt; it is just that it is the GOP that destroyed the moral and fiscal rules that used to govern the public finances. For the modern GOP, the calculus of debt and deficits is as simple as it is cynical: They are a horrible, immoral scourge… if there is a Democrat in the White House.

The past four years have been a case in point. After all, how could an extra trillion dollars be a bridge too far for Republicans who had pushed through a $1.5 trillion tax cut in 2017 for little ostensible reason other than to enrich their donor base? Nor had any of them uttered a word of protest as Donald Trump, who campaigned on a promise to pay off the national debt in eight years, instead ramped it up by nearly $8 trillion in four – the largest increase in the national debt relative to the size of the economy of any U.S. president other than George W. Bush or Abraham Lincoln. They were on board as Congress appropriated $3.5 trillion in COVID-19 relief last year, on top of the $3.9 trillion made available by the Fed to shield corporate America from the turmoil unleashed by the pandemic.

But for that sordid history, the concerns raised by the group of ten about the Biden proposal might have gotten traction with colleagues across the aisle. That Republicans have become deficit hawks now that a Democrat is in the White House may be the height of hypocrisy, yet the word ‘trillion’ does have a way of spooking some people. Centrist Democrats, who assumed the role of debt scolds as Republicans retreated from their historical role as the grownups in the room on fiscal matters, continue to express trepidation about the sheer scale of the Biden proposal. Many fear that further stimulus spending could revive long-dormant inflation and question where the endgame lies with respect to the escalating national debt, while others simply suggest that limited debt resources would best be spent on infrastructure investment.

With vaccinations accelerating, a flicker of light visible at the end of the pandemic tunnel, and already-massive sums of Covid relief dollars flowing into the economy, estimates for economic growth have risen to the 6-7% range. Inflation concerns reflect an assessment of “output gaps,” which refer to the size of the economic hole that fiscal stimulus is designed to fill when an economy is underperforming. To the extent that the Biden plan exceeds the size of the current projected “output gap,” theory has it, those excess dollars will push the country into an inflationary spiral.

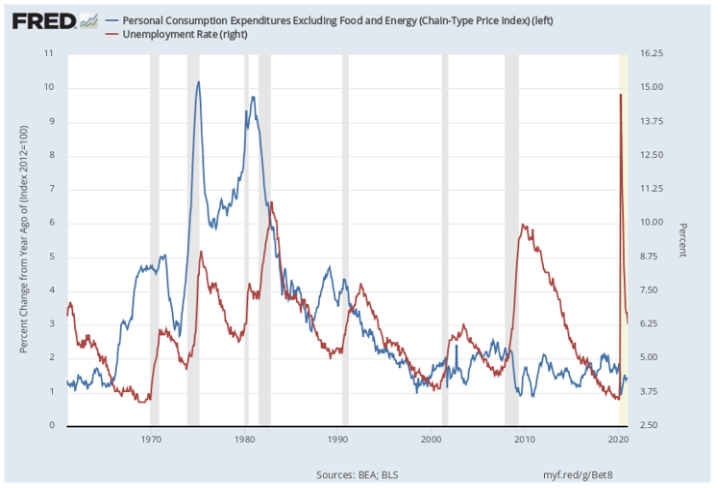

If inflation fears are met with skepticism, however, there is good reason. Time and again, over the past several decades, many economists warned that inflation lay on the horizon, pointing to deficit spending, expansive monetary policies, and plummeting unemployment rates as factors that economic theory dictates must each ultimately lead to inflation. Indeed, federal deficits have averaged over $650 billion a year over the past twenty years – and closer to a trillion dollars a year over the past ten – driving the federal debt held by the public from $3.5 trillion to over $20 trillion. Over the same time period, the Fed has pushed interest rates toward zero across the yield curve and flooded dollars into the economy at any sign of trouble. Yet, despite all that, and unemployment falling to historically low levels, the Consumer Price Index has remained in the low single digits for 30 years. Indeed, the Fed has struggled to push inflation up to its 2% target.

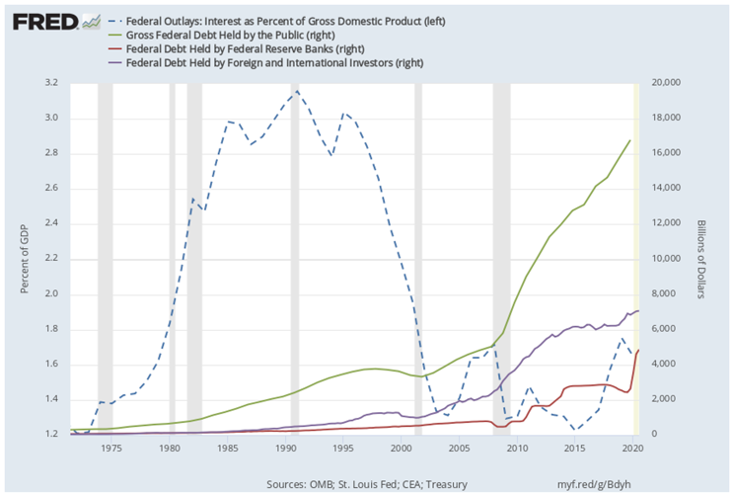

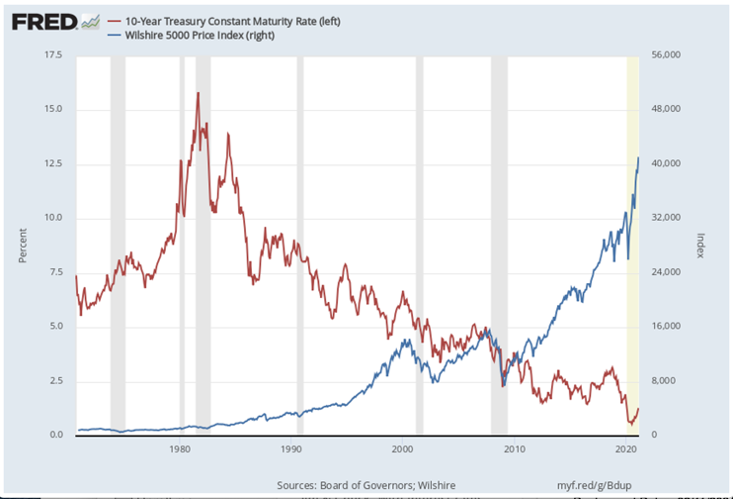

Warnings of the consequences of our growing national debt similarly did not pan out as feared. In the wake of the Reagan tax cuts in the 1980s, growing federal deficits and federal borrowing were expected to lead inevitably to higher interest rates, ballooning interest costs in the federal budget, and squeezing out private investment. Instead, as long-term interest rates declined steadily over the ensuing decades, the interest cost on the national debt remained remarkably steady in dollar terms, and declined as a share of GDP. After reaching a peak of 3.2% of GDP in 1991, net interest costs in the federal budget declined dramatically, even as the national debt continued to grow, ultimately reaching a low of 1.2% of GDP in 2015. The Congressional Budget Office now projects that the interest cost on the federal debt will remain under 2% of GDP until the 2030s, despite federal deficits continuing to exceed a trillion dollars a year and a doubling of the federal debt over the next decade. Even fears that we were doomed to be increasingly dependent on China to finance our deficits as the national debt continued to rise have proven to be unfounded. While China remains one of the two largest holders of Treasury bonds – Japan is now the largest – Treasury yields remain near historically low levels, despite China’s not having increased the dollar amount of its holdings since 2012.

It has not been lost on a lot of Americans that economic policies over recent decades – whether intentionally or incidentally – have served to enrich the wealthiest Americans. In the wake of the 2008 financial crisis, both the Occupy Wallstreet movement on the left and the Tea Party movement on the right were animated by Wall Street bailouts. Both Donald Trump and Bernie Sanders ran for President in 2016 arguing that the system was rigged – and so it was. While inflation has remained low over the past quarter-century as measured by the Consumer Price Index, inflation in asset prices has been rampant, as declining interest rates have pushed up the value of real estate, stocks, bonds, and other financial assets dramatically, increasing the net worth of America’s wealthiest families.

While much attention has been paid to growing income inequality in the United States, disparities in wealth are even more pronounced. According to data from the National Bureau of Economic Research, from 1983 to 2016, the average net worth of the top 1% of households grew from $10.6 million to $26.4 million in real terms, an increase of 150%, and the top 0.1% of households grew from $43.3 million to $100.1 million in real terms, an increase of 133%. In contrast, the bottom 40% of the population saw their 1983 net worth of $6,900 decline to a negative net worth of ($8,900) over the same period. Looked at another way, in 2019, according to the Federal Reserve Bank of St. Louis, the bottom 50% of families – roughly 64 million families – had an average wealth of $22,000, which represented only 1% of total U.S. household wealth. This compared to $411,000 for the next 40% of families and $5,716,000 for the top 10%.

“You all just got a lot richer,” Donald Trump told his friends as he arrived at Mar-a-Lago over Christmas in 2017, just days after he had signed his $1.5 trillion tax cut into law. There had been no economic rationale for the tax cuts. The economy was already steaming along, and there was no material “output gap” to be filled. Yet none of those gathered at Mar-a-Lago admonished the then-President about the possible downstream inflation that the $1.5 trillion of economic stimulus might produce or ragged on him about tacking an additional 10% onto the national debt.

And, of course, Susan Collins and her colleagues who met with Joe Biden in the Oval Office, voted for those tax cuts, and never once suggested that they would stand their ground and vote no because $1.5 trillion was just too much.

Against that backdrop, no one should be surprised that 68% of Americans support the $1.9 trillion Biden plan, as the latest Quinnipiac poll suggests. Or that 78% – including 64% of Republicans – support the proposed $1,400 stimulus checks.

Could inflation be a problem? Perhaps, perhaps not. Is the national debt looming down the road? Surely. But for most Americans, apparently, the answer is simple. Someone is putting money into their pockets this time around, and they are all for it. Republicans complaining about Democrats doing something that is too big and too wasteful might consider the irony of their stance, and perhaps rethink their opposition to the Biden plan. After all, 68% of Americans supporting anything is the closest thing to unity we have seen in a long time.

______________________________________________________________________________________________________________________

David Paul

David Paul is the founder and President of the Fiscal Strategies Group, a financial advisory firm specializing in municipal and project finance. Prior to forming the Fiscal Strategies Group, Dr. Paul was a Managing Director and member of the Board of Directors of Public Financial Management, Inc. Dr. Paul also served as the Vice Provost of Drexel University, and as the CEO of Mathforum.com, a mathematics and math education website and virtual community that is now part of the National Council of Teachers of Mathematics.

Dr. Paul is the author of When the Pot Boils: The decline and turnaround of Drexel University, and has published regular commentaries on politics and economics on The Huffington Post and Medium, and at appalled.blogspot.com.

______________________________________________________________________________________________________________________