No, not the fight against inflation, which has been front-page news for months now. That battle has certainly been on Powell’s mind; but behind the scenes, a different war has been raging for the better part of the year, this one between the Federal Reserve and Wall Street. It has been the battle to convince the elite cadre of professional money managers and stock and bond traders whose decisions drive markets on a day-to-day basis that Jerome Powell is the second coming of Paul Volcker – the legendary Fed chair who crushed post-Vietnam War inflation by boosting interest rates well into double digits and casting the nation into a deep recession. And it has been a titanic struggle, with trillions of dollars and Powell’s legacy on the line.

For decades now, Wall Street traders and deep-pocketed investors have come to rely on the Fed to step in and make sure that stock market downturns, when they happen, do not get out of hand. Dating back to Alan Greenspan’s appointment as Fed chair in 1987, the Fed has been enamored of the “wealth effect,” which suggests that the Fed should step in – meaning reducing interest rates and pumping money into the system – should stock market declines hit the 20% threshold, or thereabouts. The notion was that it was in the broad public interest to make sure that the loss of wealth among the investor class did not become severe enough to adversely impact the rest of the economy.

The wealth effect, in other words, was essentially trickle-down economics stood on its head: if a rising tide was presumed to lift all boats – a core tenet of modern capitalism – it only made sense that rough seas could sink all boats. And from such logic was birthed the Greenspan “Put” – a term that encapsulated the belief on Wall Street that when push came to shove, the Federal Reserve would step in to stem market losses (in the manner of a “put” option, a type of investment product that can insulate investors from declines in the price of a stock).

Over the ensuing decades, belief in the Greenspan Put (subsequently renamed the “Fed Put” as Greenspan’s policies were embraced by subsequent generations of Fed leaders) has been pervasive. Indeed, Jerome Powell made his bones as Fed chair through his remarkable performance in early 2020, when stock markets were collapsing as the implications of the novel coronavirus first became apparent. Faced with deepening market turmoil, Powell drew from the playbook created by then-Fed chair Ben Bernanke in response to the 2008 global financial crisis and used all the tools at the Fed’s disposal to keep money flowing through the economy.

And it worked: in the wake of a 30% decline in the S&P 500 from mid-February to early March 2020, the Fed moved aggressively to stabilize the financial markets. By the end of May, the stock market declines had largely been reversed, and even as Covid-19 shutdowns wreaked havoc across the economy, the flood of liquidity pumped into the system by the Federal Reserve marked the beginning of a new bull market, and bond and stock markets alike soared to new historic highs.

While the Fed’s performance in 2020 was widely hailed, it set the stage for the struggle between Powell and Wall Street that played out over the course of the past year. When inflation emerged as the new scourge facing the country, Jerome Powell pivoted from the Ben Bernanke playbook and sought to remake his identity as a stern inflation fighter in the model of Paul Volcker. But as much as he tried to insist that the era of the Fed Put was over, stock and bond traders did not buy it. Instead, they took Fed interest rate hikes this year in stride, and every time Powell or one of his colleagues on the Fed Board of Governors went public to insist that they were serious about pushing up interest rates to tackle inflation, a day or two of market losses were inevitably followed by market rallies, as traders remained confident that when the time came, the Fed would reverse course and bring interest rates back down.

After a battle that continued back and forth for most of the year, Powell finally prevailed two weeks ago. With the Fed’s latest three-quarters-of-a-point hike in interest rates, and continued quantitative tightening (Fed-speak for selling long-term bonds to force long-term interest rates higher) pushing mortgage rates to the highest level since before the 2008 financial collapse, traders threw in the towel. Bond and equity markets tumbled, and market indicators turned broadly negative, suggesting a widespread expectation that the economy will experience a recession of some duration, and that the Fed will not pivot to bring interest rates back down until 2024 at the earliest.

If Jerome Powell had a credibility problem, it was of his own making. He came late to the conviction that inflation was a problem that needed to be tackled with strong medicine, as for most of 2021 he argued that inflation was a “transitory” problem that would resolve itself in time. But the irony of his efforts to channel Paul Volcker as his inflation-slaying role model ran far deeper.

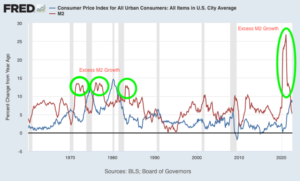

After all, Volcker was picked to lead the Fed by Jimmy Carter to tackle inflation which had become a chronic problem in the wake of the sustained expansion of the money supply by the Fed over the decade preceding Volcker’s appointment. The pattern of double-digit growth in the money supply that Volcker inherited is highlighted in the graph here, which tracks the “M2” supply of money in the economy against inflation, as defined by the Consumer Price Index. On the far right side, the graph also illustrates the far more dramatic growth in the money supply in 2020, when the Fed’s coronavirus response led to a massive increase in the money supply.

The expansion of the money supply under Powell’s leadership had no precedent in recent history. As much of the country shut down in 2020, the Fed pumped $5 trillion into the economy, ultimately resulting in a 40% increase in the money supply. By way of comparison, in the wake of the 2008 financial collapse, the increase in the money supply barely exceeded 10% in any one year. In the view of monetarists – economists who view growth in the money supply as the most important factor leading to inflation – it was only a matter of time before this massive increase in the money supply impacted price levels across the economy. In simple terms, they would argue that Jerome Powell is now fighting a problem of his own making.

Yet over the course of the Fed’s battle with inflation, Powell has had little or nothing to say about the expansion of the money supply on his watch. When questioned during Congressional hearings in early 2022 on the potential consequences of the substantial expansion of the money supply in 2020, Jerome Powell demurred. In the new world order of financial innovation, he argued, the linkages between the money supply and inflation are no longer as clear as it once was. Instead, in testimony before the Senate Banking Committee, he embraced the widely held view that current inflation had been unleashed by the combination of the impact on energy and commodity prices of Putin’s invasion of Ukraine and global supply chain disruptions caused by the Covid-19 pandemic.

Powell’s ardent advocacy for expanding the money supply to address the coronavirus problem made his subsequent insistence for much of 2021 that inflation was a “transitory” problem that would go away of its own accord all the more puzzling. Traditionally, there is a considerable time lag between monetary policy actions taken by a central bank, and when the impact of those actions ripple across the economy – whether those efforts are targeted at stimulating the economy, which the Fed sought to do by expanding the money supply in 2020, or stemming inflation as it is now seeking to do. And the emergence of inflation in the second quarter of 2021 appeared to be a case in point, as the first surge in the rate of inflation – 2.6% to over 5% from March to July 2021 – came right within the nine to eighteen-month time lag that monetary economists would predict from when the Fed began expanding the money supply in early 2020, to when it began to impact price levels. Whatever other factors were present – Putin’s war and global supply chain issues – it is hard to imagine that as a central banker responsible for monetary policy, Powell would not have expected that increasing the money supply by 40%, as the Fed did in 2020, would not have some degree of inflationary impact a year or two down the road.

Jerome Powell is an enigma. Four years ago, in a quieter moment, he compared Fed policymaking to walking through a room full of furniture in the dark, “What do you do? You slow down. You stop, probably, and feel your way.” Managing a complex modern economy with the blunt tools available to a central banker, his words suggest, is an art, as much as a science, complicated by the long lag time between actions and effects.

Then the crises hit. First Covid-19, and then inflation, and that notion of feeling your way along seemed to have fallen by the wayside. In 2020, the previously stoic, cautious Jerome Powell morphed into a sort of Ben Bernanke on steroids, as his notion of carefully feeling his way along gave way to an aggressive “go big, go fast” philosophy, and a 40% increase in the money supply – four times the rate of growth Bernanke oversaw in 2008. Now, having embraced his Volckerian persona, Powell has again left his “slow down, feel your way” stance in the rearview mirror. Once again, it is pedal-to-the-metal, just heading in the opposite direction this time.

History may not treat Powell well. Interviewed last week, long-time Wall Street wizard Carl Icahn offered a harsh retort to Powell’s newfound embrace of Paul Volcker, as Icahn compared the Fed’s expansion of the money supply in 2020 to the debasement of the currency that brought about the fall of the Roman Empire. Others fear that in his zeal to tighten the economic screws, there is a real possibility that Powell will overshoot to the downside this time, and leave the nation trapped in a deflationary spiral.

In the end, it is not the extremes of Powell’s actions that are difficult to comprehend, as the challenges he has faced are truly historic, but the refusal to acknowledge the potential unintended consequences of his actions, as the nation is whipsawed from one crisis to the next. Perhaps this will not be the end of the world as we know it, as Icahn suggests, but while Jerome Powell continues to try to reframe his persona in the heroic image of Paul Volcker, a more apt analogy may be the arsonist who hops on the fire truck and seeks to lead the effort to put out the blaze, hoping beyond hope that no one will notice the box of matches in his back pocket.

_____________________________________________________________________________________________________________________

David Paul is the founder and President of the Fiscal Strategies Group, a financial advisory firm specializing in municipal and project finance. Prior to forming the Fiscal Strategies Group, Dr. Paul was a Managing Director and member of the Board of Directors of Public Financial Management, Inc. Dr. Paul also served as the Vice Provost of Drexel University, and as the CEO of Mathforum.com, a mathematics and math education website and virtual community that is now part of the National Council of Teachers of Mathematics. Dr. Paul received a BA in economics from Yale University, an MBA in Finance from the Wharton School, and a doctorate in Higher Education Management from the University of Pennsylvania. Dr. Paul is the author of When the Pot Boils: The decline and turnaround of Drexel University, and has published regular commentaries on politics and economics on The Huffington Post and Medium, and at appalled.blogspot.com.